The Golden Handcuffs Solution

Why Refinancing in 2025 is a Mathematical Mistake (And What to Do Instead)

Context: The “Lock-In” Effect We are currently living through one of the strangest mortgage markets in history. Between 2020 and 2021, millions of Americans locked in 30-year fixed mortgages at historic lows of 2.5%, 3%, or 4%. Today, in late 2025, rates are hovering significantly higher.

This has created what economists call the Lock-In Effect. You might have $200,000 in equity sitting in your house that you want to access for renovations or debt consolidation, but you feel handcuffed to your home. You cannot sell, and you cannot refinance, because losing that 3% rate feels like financial suicide.

Why This Is a “Must-Read” Strategy If you need cash, the traditional move was always a Cash-Out Refinance. But in 2025, that move is dangerous. When you do a Cash-Out Refi, you are taking your entire mortgage balance—not just the cash you want—and moving it to the new, higher interest rate.

The solution is the HELOC (Home Equity Line of Credit). It allows you to keep your primary mortgage exactly where it is and only pay the current market rate on the specific cash you borrow.

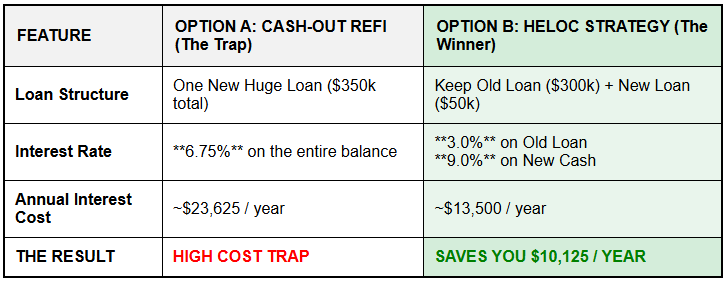

The Side-by-Side Comparison Let’s look at the numbers. We compared two scenarios for a homeowner who needs $50,000 for renovations.

Scenario A is a traditional Cash-Out Refinance.

Scenario B is the HELOC Strategy.

As the chart above shows, even though the interest rate on the HELOC looks higher on paper, the effective cost is dramatically lower. By keeping your original low-rate mortgage, you save over $10,000 per year in interest payments.

5 Things You Probably Didn’t Know About HELOCs

The Fixed-Rate Partition Most people fear HELOCs because they have variable rates. However, most modern HELOCs allow you to partition your balance. You can take that $50,000 draw and lock it at a fixed rate for 5, 10, or 20 years, effectively turning it into a fixed second mortgage while leaving the rest of your line of credit open and available.

Interest Can Still Be Tax-Deductible There is a myth that HELOC interest is no longer deductible. Under current tax law (through 2025), you can still deduct the interest on a HELOC, provided the funds are used strictly to buy, build, or substantially improve the home securing the loan. Always consult your tax professional, but do not assume the deduction is gone.

It Functions Like a Giant Credit Card Unlike a loan where you get a lump sum and start paying interest immediately, a HELOC is revolving. You do not pay interest on the money until you actually touch it. If you get a $100k line of credit but only use $10k for a bathroom remodel, you only pay interest on the $10k.

The Reset Shock is Real HELOCs usually have a 10-year Draw Period (interest-only payments) followed by a 20-year Repayment Period. When the clock hits year 11, your payment will jump because you are suddenly paying principal plus interest. You must plan for this date.

Banks Can Freeze Them A HELOC is a revocable line of credit. If your home value drops significantly or your credit score tanks, the bank has the right to freeze your access to the funds. It is smart to draw what you need for big projects sooner rather than later.